Sydney just posted its worst auction clearance in more than six years. Melbourne's clearance rate is at its weakest since the 2021 lockdowns. Properties are being withdrawn from auction rather than sold below vendor expectations. And Domain is forecasting falls of 3 to 7% in Sydney and 4 to 8% in Melbourne through the rest of this financial year. The pitch writes itself: at last, a break for first home buyers.

It is not that simple, and lending is the first reason why. Credit has tightened sharply. Banks are pulling finance, cutting how much buyers can borrow, and still testing every new loan at around 9%, well above the rate a borrower would actually pay. Even a buyer who has saved a deposit cannot borrow enough to meet what vendors are asking. And the deposit schemes Labor is promoting do not fix that wall. They load buyers with more debt, more government strings, and more downside risk at the worst point in the cycle.

That is the first wall. The second is that Labor set its key help, the stamp duty exemption and the 5% deposit scheme, below what a home in Sydney actually costs, so even a buyer who can borrow is locked out. Here is what is actually happening, and why the market has locked up.

The deposit door opened, the income door stayed shut

The same thing pulling prices down is also shrinking your loan. Rate rises since February have lifted the cash rate to 4.10%, and Domain's chief economist Nicola Powell estimates the average household has lost 7 to 8% of its borrowing power as a result. So as prices fall a few per cent, the maximum you can borrow falls by about the same. The two cancel each other out, so it's all relative.

On top of that, the APRA serviceability buffer is still 3 percentage points. Banks test whether you could repay at roughly 9%, not the 6% or so you would actually pay. That buffer, not the sticker price, is what knocks most first home buyers back. A cheaper house you still cannot get the loan for does not help you.

Labor set the help below the price of a Sydney home

This is the trap underneath everything else. The two headline supports for first home buyers, the stamp duty exemption and the 5% deposit scheme, are both set below what a home in Sydney actually costs. The stamp duty exemption stops at $800,000. The First Home Guarantee is capped at $900,000 in Sydney. The median Sydney unit sits around $871,000 and the median house is above $1 million.

So the help only kicks in at prices Sydney does not offer. A first home buyer waiting to get under the $800,000 line is not waiting for a dip, they are waiting for a crash of hundreds of thousands of dollars. Sellers will not drop that far, buyers cannot reach up, and that standoff is exactly why clearance rates have collapsed and nothing is selling.

| Labor's threshold | Sydney reality | |

|---|---|---|

| Stamp duty exemption | Cuts out at $800,000 | Median unit around $871,000, already over the line |

| 5% deposit scheme cap (Sydney) | $900,000 | Median house well over $1 million, does not qualify |

| Cheapest Western Sydney hub | Needs to be under the caps | Penrith around $980,000, still over |

Why nothing is moving, and why it snaps back

The freeze is not random. It is a standoff with a clear mechanism. Vendors will not accept lower prices, so they withdraw, almost a quarter of scheduled auctions are now being pulled rather than sold. Investors are not dumping stock either, they are holding, because the rental market is paying them to wait. The national vacancy rate is just 1.2%, below 2% in every capital, and rents are up 7.8% over the year to a national average of $700 a week. A landlord collecting a rising rent on a scarce property has no reason to sell into a falling market.

On the other side, first home buyers are watching and waiting, for a rate cut, or for prices to slip under the $800,000 stamp duty line. Total listings have actually edged up, but the quality stock is scarce because owners of good homes are holding on. So the market is full of what people do not want and empty of what they do.

The release valve should be new builds. They carry the first home owner cash grant and a higher $950,000 scheme cap. But developers cannot deliver. Building approvals are falling, unit approvals dropped 25.7% in March, and the National Housing Accord is running 27% behind its target, with just 219,000 homes built in 15 months against the 300,000 needed. A record 3,490 construction firms collapsed in the 2024 to 2025 financial year as costs kept climbing.

That is the trap. The freeze is not fixing affordability, it is loading the spring. When rate cuts finally arrive, pent-up demand will hit a market with almost no new supply, and prices snap straight back up. The buyers waiting for the bottom will be competing all over again, at higher prices, for the same scarce stock.

The 5% deposit scheme makes the loan bigger, not the test easier

Labor's headline measure, the Australian Government 5% Deposit Scheme, dropped the income caps and place limits from 1 October 2025. You can buy with a 5% deposit and skip lenders mortgage insurance.

What Labor has not promoted as loudly is the property price cap. In Sydney, the cap is $900,000 for an existing home and $950,000 for a new one. In Melbourne it is $800,000. If the property you want is above the cap, you get nothing from this scheme. In Sydney's middle ring, where a three-bedroom house in a reasonable suburb routinely lists above $1 million, the cap shuts most buyers out entirely.

The catch is in the maths. A smaller deposit means a bigger loan, and you still have to prove you can service that 95% loan at the 9% test rate. The scheme lowers the deposit hurdle. It does not touch the serviceability hurdle, which is the one doing the damage right now.

Matt Canavan: the banks have got the yips

Nationals Leader Matt Canavan put it plainly on Sky News on 29 June 2026.

"The simple fact is fewer homes are being sold now, auction clearance rates are at record lows," he told host Paul Murray. "Our banks have got the yips, and they are pulling finance left, right and centre, lowering the amount that can be borrowed, and that is forcing a lot of people out of the market."

Canavan was direct about who pays the price. "The people that are most likely to be forced out of the market with that tightening of credit standards will be first home buyers." He also dismissed Labor's claim that schemes are delivering for buyers: "There's no evidence that first home buyers are now making up a massively disproportionate share of what are fewer homes being sold."

That is the opposition confirming what the clearance data already shows. Fewer transactions, tighter credit, and first home buyers bearing the brunt of both.

'Help to Buy' hands Canberra up to 40% of your home

Then there is Help to Buy, the shared equity scheme that opened in December 2025. You can buy with a 2% deposit, and the government takes an equity stake of up to 40% on a new home or 30% on an existing one. This is where the fine print bites.

- The income caps are $100,000 for a single buyer and $160,000 for couples and single parents. Go over the cap for two years running and you can be forced to buy back the government's share. A decent pay rise can turn the scheme against you.

- You share the upside. When the market recovers, the government's 30 to 40% slice grows too, so you hand back a chunk of your capital gain.

- There are only 10,000 places a year. It is rationed, and it is offered through a short list of lenders.

- If you renovate or improve the property, the government's equity share applies to the higher value at sale or buyout, they take their 30 to 40% cut of every dollar of increased value even though they did not contribute a cent to the works.

- Help to Buy does not exempt you from stamp duty. That is a state tax and the federal scheme does not touch it. Buy a $700,000 property in NSW under Help to Buy and you still owe roughly $17,000 in stamp duty at settlement, out of your own pocket, on top of a 2% deposit. The government takes up to 40% of your home and leaves you to find the upfront tax yourself.

The scheme launched on 5 December 2025. By February 2026, just 278 households had actually purchased a home through it, with about 2,000 more conditionally approved. That is 278 out of 10,000 available places, a 2.78% take-up rate in the first two months. Tasmania did not even join the scheme until 5 June 2026, and Western Australia only came on board on 22 December 2025, weeks before those numbers were published. Housing Australia has not released updated monthly figures since February. If the numbers were good, they would be publishing them every month. They are not.

The First Home Owner Grant: new builds only, most buyers don't know this

This is where the most common misconception sits. The First Home Owner Grant is a cash payment from the state government, but it is only available on newly built or substantially renovated homes. It does not apply to existing properties.

The amounts vary by state. In NSW it is $10,000 for new homes valued up to $600,000. In Victoria it is $10,000 for new homes up to $750,000. Queensland boosted its grant to $30,000 for new builds. Buyers who assume this cash grant applies to any first home purchase are in for a shock when they get to settlement and find they do not qualify because the home they chose was not new.

The First Home Super Saver Scheme: designed for people who don't need it

The First Home Super Saver Scheme lets you make voluntary contributions into superannuation and then withdraw up to $50,000 of those contributions to use as a home deposit. It sounds generous. The problem is who it actually helps.

To benefit you need spare cash sitting around that you can afford to lock into super on top of your compulsory contributions. The people who need first home buyer help the most are the ones already stretched paying rent while trying to save a deposit. They are not making voluntary super contributions. The scheme is designed for disciplined savers with surplus income, which is precisely the group that least needs a government hand. It is another Labor measure that looks good in a press release and misses the people it was supposed to reach.

Buying with 5% down in a falling market is a negative equity trap

This is the part the cheerful headlines skip. Buying with a wafer-thin deposit in a market that is still forecast to fall means you'll be in instant negative equity. Buyer's agent Emily Wallace of Wallace Advocates told The Age the biggest risk for buyers right now is overpaying, and warned that offering 5% over the price guide, a habit from the hot market, is "just not happening at the moment." Negative equity only bites if you refinance or sell, but it traps you the moment your circumstances change.

Stamp duty: the one accidental win Labor won't mention

Falling prices have quietly pushed more properties under the stamp duty threshold and unlike every scheme on this page, there is no debt attached, no government equity stake, no income cap and no fine print. In NSW, first home buyers pay no stamp duty on purchases under $800,000, with a concession up to $1 million. In Victoria it is no duty under $600,000.no stamp duty under $800,000The catch is Labor had nothing to do with it. The thresholds did not move. The market came down to meet them. And in Sydney's middle ring, where the median house still sits well above $900,000, most properties remain out of threshold range entirely. The stamp duty saving is real where it applies. It just applies to fewer Sydney properties than the government's messaging implies, and it required prices to fall to get there.

What it looks like in real numbers

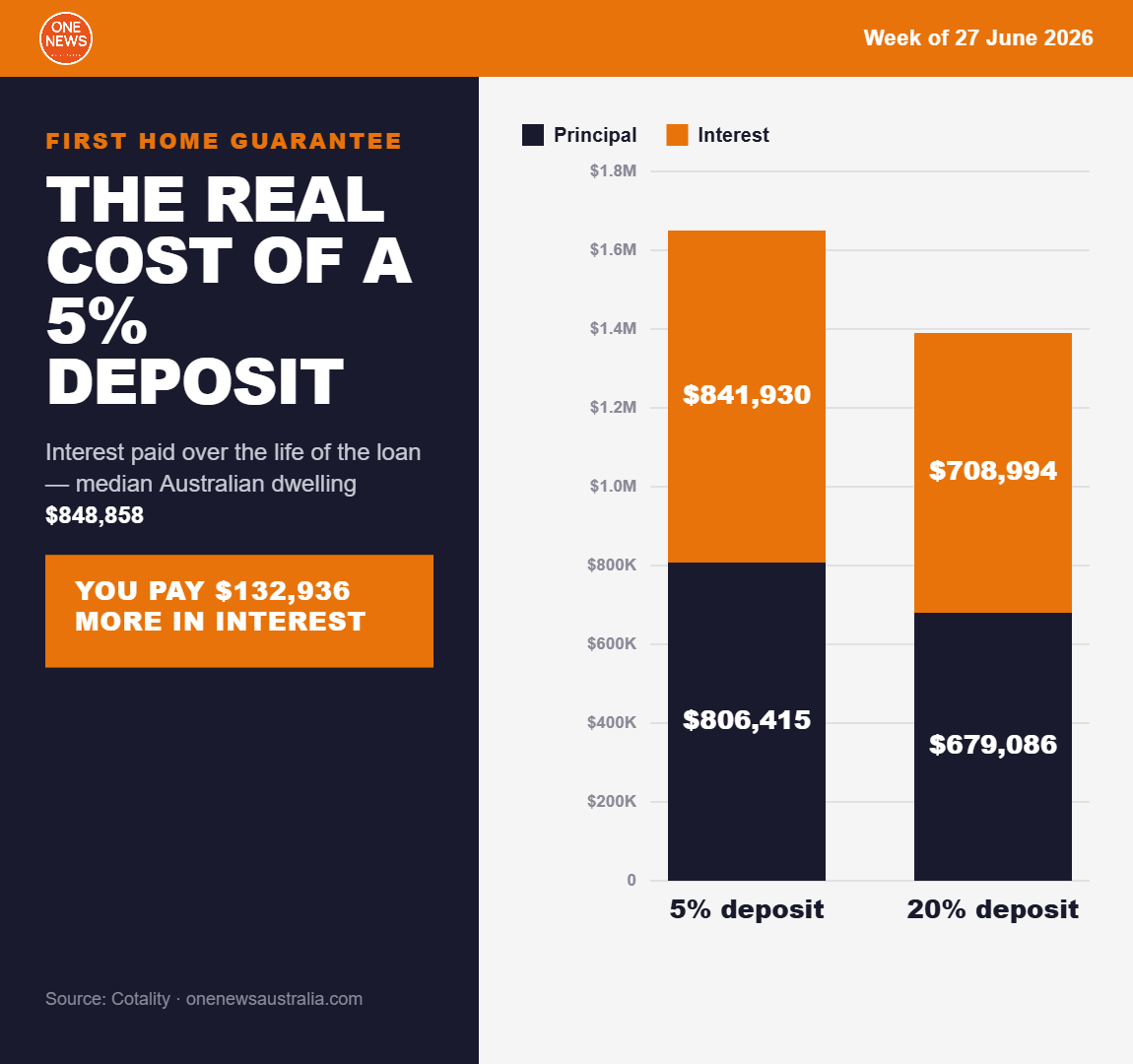

Take the median Sydney unit at around $871,000, the cheapest realistic way into the market.

| What Labor says | What it actually means | |

|---|---|---|

| The deposit | Put down just $43,500 | You then borrow $827,000, versus $697,000 for a 20% deposit buyer. You carry $130,000 more debt |

| Stamp duty | Sold as help for first buyers | The exemption stops at $800,000. A median unit is over the line and pays duty |

| Getting the loan | Easier to buy | Same 9% test, now on the bigger loan |

| Interest over 30 years | Not mentioned | Tens of thousands more than a 20% deposit |

| A house instead? | The 5% scheme is available | The median Sydney house is over the $900,000 cap. It does not qualify |

| If prices keep falling | Not mentioned | Instant negative equity. You owe more than the unit is worth |

The entry cost looks smaller. Everything underneath it is bigger: the loan, the interest, the risk. The deposit door swung open. The income door did not.

Labor's 300,000 figure is a Morrison scheme, Help to Buy has placed 278

The number Labor keeps citing, more than 300,000 Australians helped into homes, belongs to the Australian Government 5% Deposit Scheme, a Morrison government initiative that launched in January 2020, two and a half years before Labor took office. By the time Labor won the May 2022 election, the scheme had already been running for over two years and placing tens of thousands of buyers annually. Labor inherited it, removed the income caps in October 2025, and is now presenting the entire six-year cumulative total as evidence its own housing agenda is working. The one thing they actually changed was taking the handbrake off a Morrison policy that was already delivering.

Of those 300,000+, about 30,000 involved new homes built, the rest bought existing stock. More than 48,000 were permanent residents added after a July 2023 eligibility expansion. The scheme was not Labor's idea, Labor did not fund it, and the majority of its placements predate the current government.

Labor's own flagship housing scheme, Help to Buy, launched in December 2025 and has completed 278 actual purchases out of 10,000 available places. That is a 2.78% take-up rate. Housing Australia has not published updated figures since February 2026. The 300,000 number is six years of someone else's work. The 278 is Labor's own.

The average couple earns too much to qualify

There is a detail buried in the Help to Buy fine print that Labor has never once highlighted in its promotion of the scheme. The income cap for couples and single parents is $160,000 combined. Two people on the median Australian full-time wage earn approximately $196,000 combined. The average Australian couple is over the cap and cannot access the scheme at all.

The people Help to Buy actually serves are single buyers earning under $100,000 and lower-income couples where one or both partners earn below the median. Those buyers are also the most exposed to repayment stress and negative equity risk in a falling market. The scheme designed to help the most vulnerable buyers puts them into the highest-risk position with the thinnest deposit at the worst point in the cycle.

The average couple, two teachers, two nurses, a tradie and a retail worker, earns too much to qualify and too little to comfortably service a Sydney mortgage without help. Labor has not acknowledged this gap publicly. One News Australia will examine the couple scenario and what it means for middle-income households in a follow-up piece.

So when should first home buyers actually move?

Most market forecasters are pointing to late 2026 into early 2027 as the period when conditions start to improve for buyers. The trigger is rate cuts. The Reserve Bank has signalled cuts are coming, and when the cash rate drops meaningfully, borrowing power starts to recover and pent-up demand begins to unlock. Domain and PropTrack are both forecasting continued falls of 3 to 8% in Sydney and Melbourne through the rest of 2026 before prices stabilise.

The case for waiting is straightforward: better borrowing power, less negative equity risk, and more stock as frozen vendors finally accept the new price reality. The case against waiting is equally straightforward. Nobody rings a bell at the bottom. By the time it is obvious the market has turned, prices have usually already risen 5 to 10% off the floor. The buyers who waited for the bottom in 2020 missed the entire 2021 run.

The sweet spot most analysts are pointing to is mid-2027, after one or two rate cuts have improved serviceability but before the full wave of pent-up demand floods back and prices snap upward.

So who actually comes out ahead

The first home buyer who actually comes out ahead is the one who waits for a rate cut, which is not expected until late 2026, buys under the stamp duty threshold, and steers clear of the highest leverage schemes while prices are still sliding. Labor has thrown open the deposit door and called it generosity. The income door it left shut, and the risk it quietly moved onto the buyer. For the full picture on what the auctions and the polling are saying about the budget, read our analysis of Labor's budget backlash.

This article is general information only and does not constitute financial advice. Property markets are unpredictable and individual circumstances vary. Before making any property purchase decision, speak with a licensed mortgage broker and an independent financial adviser who can assess your specific situation.